From January 1, 2026, Nigeria new tax laws officially take effect. After months of debate, protests, misinformation, and policy fine-tuning, President Bola Tinubu signed four thorough tax reform bills into law in June 2025. Together, they redefine how Nigerians earn, save, invest, run businesses, and interact with the tax system.

These new tax laws in Nigeria are not cosmetic. They affect salaries, side hustles, crypto, investments, VAT, small businesses, multinationals, and even how banks report transactions. Here’s the clearest, most practical breakdown of what the new tax laws actually mean for you.

READ ALSO: All You Need to Know About the Latest FIRS–France Tax Partnership

The Four New Tax Laws You Should Know

These four major laws are the pillars of Nigeria’s tax reforms:

- Nigeria Tax Act 2025 : Merges dozens of old tax laws and removes over 50 overlapping taxes.

- Tax Administration Act 2025 : Harmonises tax collection across federal, state, and local governments.

- Nigeria Revenue Service Act : Replaces FIRS with an independent Nigeria Revenue Service (NRS).

- Joint Revenue Board Act : Establishes a tax ombudsman and appeal tribunal for disputes.

The goal is simple: fewer loopholes, clearer rules, broader compliance, and higher revenue without squeezing low-income Nigerians.

Who Is Now Taxable in Nigeria?

For the first time, the law clearly defines tax residency. A Nigerian tax resident is anyone who:

- Live or are domiciled in Nigeria

- Maintain a permanent home in Nigeria

- Spend 183 days or more in Nigeria in a year

- Have strong economic or family ties in Nigeria

- Are a Nigerian diplomat or public servant abroad

Why this matters:

The taxes on residents is on their worldwide income (with treaty reliefs) and only Nigeria-sourced income for non-residents.

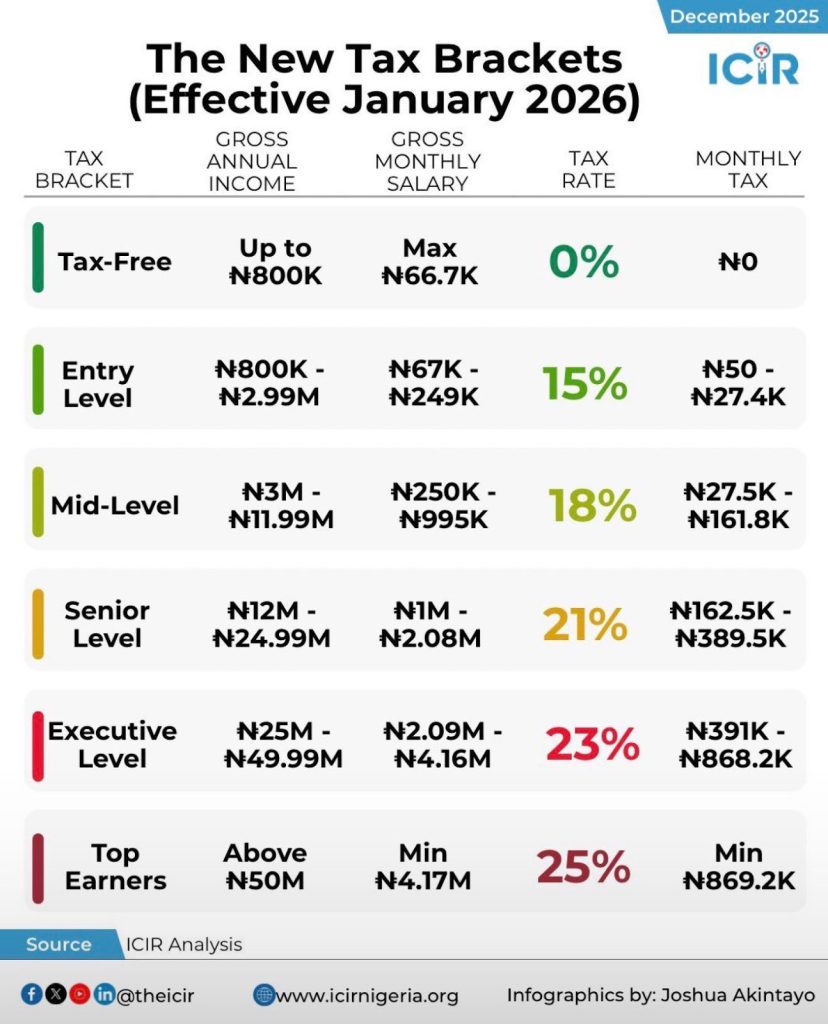

Salary Earners: Who Pays Less, Who Pays More

- ₦800,000 Is Now Fully Tax-Free

If you earn ₦800,000 or less annually, you pay zero income tax. This includes minimum wage earners.

- Progressive Rates for Higher Earners

There is progressive tax on income above ₦800,000, topping out at 25% for incomes above ₦50 million. Most middle-income earners (₦1m–₦10m) will see slightly lower effective tax rates than before.

- Bigger Relief for Job Loss

Compensation for redundancy, injury, or job loss is now tax-free up to ₦50 million, up from ₦10 million.

Investments, Crypto, and Capital Gains

- Stocks and Capital Gains

You won’t pay Capital Gains Tax (CGT) if your annual share sales are below ₦150 million, and your total gains are ₦10 million or less. Above this threshold, your personal income tax rate applies on your gains.

- Crypto Is Now Taxable

Crypto, NFTs, and digital assets are officially classified as taxable assets.

- Holding crypto: no tax

- Selling at a profit: taxable

- Staking rewards: taxable

Small Businesses, Freelancers, and SMEs

- ₦100 Million Turnover Threshold

Businesses earning below ₦100 million remain exempt from Company Income Tax.

- Development Levy Explained

A 4% Development Levy applies only to larger companies and replaces multiple old levies (TETFund, IT Levy, NASENI, Police Trust Fund). Small businesses are exempt.

Value Added Tax (VAT): What Changed and What Didn’t

- VAT rate stays at 7.5%

- There’s zero rating on essentials like food, medicine, education, and electricity, not just an exemption

- Businesses can now recover input VAT

- E-invoicing becomes mandatory from 2026, with phased rollout

Banks, Reporting, and Compliance

Banks must now report individual accounts with ₦25 million+ monthly transactions and corporate accounts with ₦100 million+ monthly transactions. No taxes on your balance, only your actual income.

Penalties have also increased:

- Late filing: ₦100,000 first month

- Contracting unregistered vendors attracts ₦5 million fine

What Nigerians Are Saying

There’ve been mixed online reactions. Some Nigerians welcome the reforms, especially the ₦800k tax-free threshold and VAT relief on essentials. Others worry about increased surveillance, bank reporting, and crypto taxation that might have adverse effects.

Experts agree on one thing: implementation will decide whether this reform succeeds or fails.

Bottom Line: What You Should Do Now

- Review your income and tax exposure before 2026

- Update payroll, records, and documentation

- Prepare for e-invoicing if VAT-registered

- Keep clean records for investments and crypto

Nigeria’s tax system is changing, not to punish, but to formalise. For most Nigerians earning modest incomes, the reforms reduce pressure. For high earners and large businesses, the net is tighter.

Either way, ignorance will be costly in 2026.